Terms like “deferred revenue” can confuse non-accountants, but the concept is easy enough. Deferred revenue and deferred revenue tax treatment means that when customers pay upfront for products or services, they will receive later, your accountant recognizes that income over time rather than all at once.

In this article, we’ll explain the GAAP-compliant method of reporting, provide bookkeeping examples, and explain how the practice will impact your taxes.

Table of Contents

Indinero’s business tax services are here to help. We’ll handle the accounting details so you can focus on what you do best.

For more details on GAAP compliance, click below to download our free essentials checklist.

Tax Treatment of Deferred Revenue

Businesses must report deferred revenue as taxable income when cash is received, even though accounting standards treat it as a liability. This creates timing differences between book and tax reporting. The IRS requires immediate recognition of advance payments, while GAAP defers revenue recognition until performance obligations are satisfied.

Deferred Revenue Accounting Principles

Since deferred revenue is an aspect of accrual accounting, let’s begin by distinguishing between the two primary accounting methods. Our cash vs. accrual accounting article covers the topic in-depth, but here’s a quick refresher.

The difference between these two approaches comes down to timing. With cash accounting, revenue and expenses are recognized when money enters or exits your bank account. Accrual accounting, on the other hand, recognizes revenue and expenses when committed to, regardless of when money changes hands.

When deferred revenue is recorded, it represents a financial liability on the balance sheet to represent the cost of a service yet to be delivered.

Why Use Deferred Revenue Reporting Over Cash Accounting?

Cash accounting is certainly simpler, so why would businesses add complexity?

There are a few reasons:

- It aligns with GAAP, which publicly traded companies must adhere to.

- Under GAAP, it is considered a “conservative accounting” practice. In contrast to “aggressive accounting,” where one-time revenue injections can overstate company valuations, deferred revenue ensures investors and creditors aren’t misled.

- Deferring revenue means matching income with related expenses, which helps financial statements report company profitability more accurately.

- While revenues can appear volatile in cash accounting, this technique smooths income fluctuations and provides a more stable, representative picture of financial performance.

- It allows companies to strategically time income to maximize tax benefits.

The Journal Entry

In accounting, “journal entries” are records of financial transactions; they’re how businesses track revenue and expenses. When using deferred revenue, your journal entries will look a bit different.

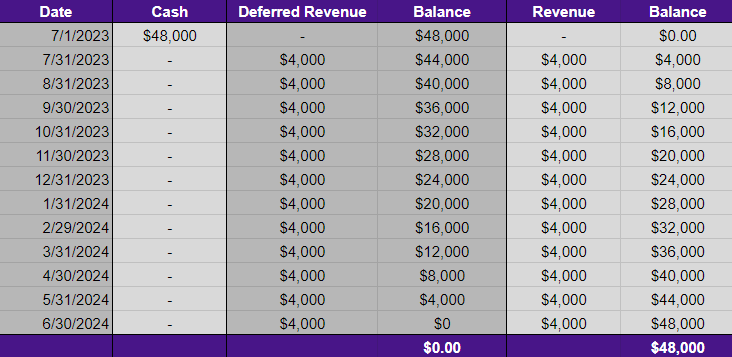

Let’s continue with our SaaS company example. In addition to providing an example journal entry, we’ve set the dates to straddle two calendar years to demonstrate how deferred revenue reporting impacts taxes.

Our hypothetical software company has signed a year-long maintenance contract for $48,000, which will be paid in full on July 1st.

Let’s walk through this example:

- After being paid, they record $48,000 in their cash account and create a corresponding entry in their deferred revenue balance.

- Each month, the company debits (decreases) this account and credits (increases) the revenue record by $4,000 (one-twelfth of the original payment).

- The cash account doesn’t change after the initial payment.

- After twelve months, the revenue balance fully reflects the $48,000 payment, while deferred revenue has been reduced to zero.

- Since the revenue is recognized over two tax years, despite receiving an upfront payment, the company will report taxable revenue to the IRS over these two years.

FAQs

Is Deferred Revenue a Liability?

Yes, according to GAAP standards, it is recorded as a liability on a company’s balance sheet.

Is Deferred Revenue an Asset?

No, it is not recorded as an asset. When a company receives an upfront payment, its cash account will reflect this, but the corresponding deferred revenue is listed as a liability.

Is It Always Recognized Evenly Over the Subscription Period?

No, the recognition of deferred revenue can vary. Some may recognize it evenly, while others use milestone achievements or project triggers for recognition; it depends on what method most accurately reflects service delivery.

Can Deferred Revenue Be Used in Cash Accounting?

No. Cash accounting focuses on cash movements; recognizing revenue based on obligations and service delivery dates is a principle of accrual accounting.

Conclusion

Deferred revenue, a component of accrual accounting, aligns with GAAP principles, providing a conservative and transparent approach to financial reporting. Unlike cash accounting, deferred revenue recognizes income in line with service delivery rather than when cash payments are received.

The practice promotes transparency for investors, more accurately matches income with associated costs, and carries important implications for the timing of tax burdens.

For help with GAAP-compliant accrual accounting, indinero’s accounting services are here to help.

{kind=link}