The home office deduction can help business owners or remote workers cut back on their tax bills — but figuring out if you qualify or how to apply it can be challenging.

In this guide, you’ll learn:

Table of Contents:

If this guide does not answer a tax deduction question, skip the Google labyrinth and try our ultimate business tax deductions guide or consult the IRS source documentation on the home office deduction.

If you’d prefer to avoid the hassle and want more time to focus on what you do best, consider indinero’s business tax services.

What Are the IRS Rules for the Home Office Tax Deduction?

The IRS uses several qualifications to determine who is eligible for home office deductions. In short, to qualify, you must:

- Be a business owner or freelancer

- Use your home as your principal place of business

- Use the space in your home exclusively for business

- Use the space for work regularly

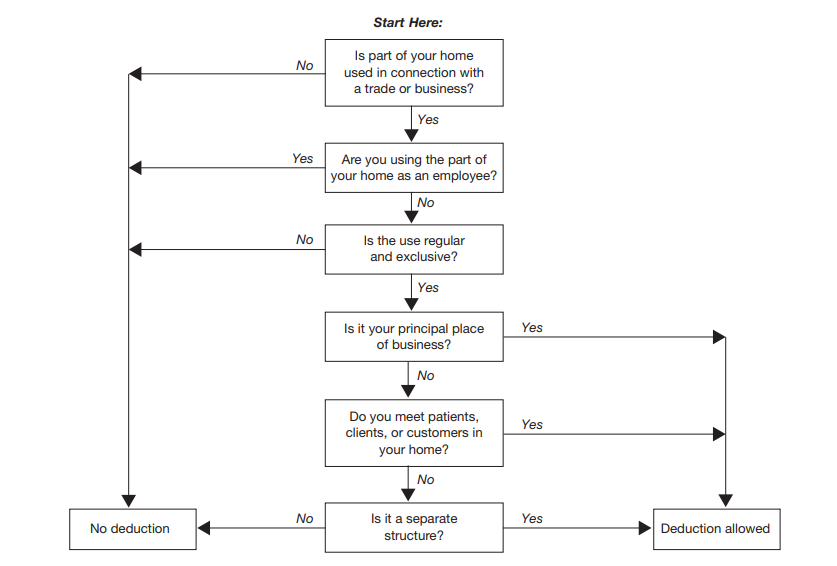

Below is the flowchart that the IRS and professional CPAs use to determine eligibility. We’ll provide clarification on definitions and details for each step below.

Is part of your home used in connection with a trade or business?

This may seem obvious, but to claim the home office tax deduction, you must dedicate part of your primary home to work. W-2 employees are not eligible for the deduction as part of that work.

Freelancers, independent contractors, sole proprietors, and single-member limited liability corporations can deduct home office expenses.

If you’re unsure if this includes you, the signature characteristic of these groups is that they are responsible for paying their own federal and state taxes. Additionally, businesses cannot dictate how, when, or where the work is done.

Some businesses reimburse home expenses, but that’s not an IRS matter.

Are you using the part of your home as an employee?

W-2 employees who freelance outside of work can qualify for the deduction, but if they work from home, the spaces used for their job and their freelancing must be distinct to qualify for the deduction.

Is the use regular and exclusive?

The IRS is serious about making sure people who claim the home office deduction are using the space as they claim. The following two pass-fail tests are how.

Exclusive use test

In order to separate personal and business spaces, you don’t need a door or other permanent partition. It simply needs to be a separately identifiable space.

For example, let’s say you’re a marketing agency owner and work from your kitchen table. Since you also cook and eat in this space, it is not used exclusively for business, and you cannot claim a business deduction.

However, if you placed a desk and other office furniture in a portion of your kitchen and use that section only for business, this would be eligible for the home tax deduction.

Exception 1 – inventory storage

If you work in wholesale or retail sales and store inventory at home, that storage space can be multipurpose, not distinct as outlined above. So if you’re using a portion of a garage, attic, or shed for inventory, it would qualify for the home office deduction.

Exception 2 – daycare facilities

Workers who care for children, people over 65, or those unable to care for themselves may mix personal and business spaces and remain eligible for this deduction. Qualifying businesses must have an official state-provided license for their work.

Regular use test

To claim the home office deduction, business owners must regularly use the space for work.

However, the IRS language around the word “regular” is unclear, and they don’t specify how much time you need to be working in the space to consider it “regularly.” In this case, ask a tax professional or use your best judgment.

The IRS stipulates that if the space is only used for a period of months rather than the whole year, you’re only eligible for the time that the space was being used.

So if you started your business midway through the year, or were a W2 employee freelancing on the side for a portion of the year, make a claim only for the time you used.

Is it your principal place of business?

IRS guidance considers managerial and administrative duties as the most substantive proof of the principal place of business test. These most relevant activities include:

- Billing customers, clients, or patients

- Keeping books and records

- Ordering supplies

- Setting up appointments

- Forwarding orders or writing reports.

You can have multiple locations where you carry out these activities, but if you want your space to qualify for the home business deduction, it must be where you do most of this work.

The examples the IRS provides for this test reveal a significant degree of leniency.

For instance, electricians who do what most would consider their most crucial work on-site can still qualify for the deduction if their home is their administrative hub. In another example, they write that a self-employed anesthesiologist who does most of their work in hospitals but administrative duties from home would also qualify.

Do you meet patients, clients, or customers in your home?

If you don’t do much administrative work at home but regularly meet clients there, your workspace will also pass the principal place of business test.

The IRS includes this illustrative example:

“A self-employed attorney works three days a week in their office, then works two days a week in a home office used only for business. They regularly meet clients there. The home office qualifies for a business deduction because they meet clients there in the normal course of their business.”

Is it a separate structure?

Should your home not be a principal place of business nor where you regularly meet clients, this is the last test that may qualify you for the deduction.

If you use it exclusively and regularly for your business, you can deduct expenses for separate free-standing structures, such as a studio, workshop, garage, or barns.

The most obvious use of separate structures is for storage, but you’re eligible if you’re conducting legitimate business with the freestanding structure.

How To Calculate the Home Office Deduction

There are two methods for calculating the home office tax deduction. You can use whichever one brings you more value.

Business Use of Home: Simplified Method

This method is also known as the home office safe harbor.

Measure the size of the space and multiply each square foot by $5. The maximum square footage for this method is 300, and the most you can deduct in a year is $1500.

Business Use of Home: Real Expense Method

The real expense method deducts actual expenses, including mortgage interest, insurance, utilities, repairs, and depreciation, based on the percentage of the home space used exclusively and regularly for business purposes.

Here’s a chart breaking down the degree of deductibility for home office expenses organized by direct, indirect, and unrelated expenses.

| Expense | Definition | Examples | Deductibility |

| Direct | Expenses only for the business part of your home | Office supplies, furniture, filing cabinets, technological equipment, repairs, or upkeep specific to the space | 100% of the value is deductible |

| Indirect | Expenses for keeping up your entire home | Insurance, property taxes, utilities, rent, repairs, and mortgage payments** | Proportionally deductible based on square footage of space dedicated to work |

| Unrelated | Expenses exclusively for portions of your home not used in business | Lawn care, painting or furnishing other spaces, entertainment devices | Not deductible |

Note: Mortgages and rent are treated differently. Renters may use the cost of rent as their calculation basis. Homeowners may not deduct the fair rental value. They must use the depreciation method. See below for instructions on calculating depreciation.

FAQs About the Real Expense Method of the Home Office Deduction

The real expense method is considerably more complicated than the safe harbor approach, so we’ve broken down some commonly asked questions:

Does the real expense method have a square footage cap?

No.

If the space complies with the qualification criteria, you may claim as many square feet as you use.

Does the real expense method have a deduction limit?

Yes.

Calculate your gross income minus business expenses: This is the maximum amount you may deduct under the real expense method.

In other words, you can’t deduct more than your profit. For more, see our article on calculating Gross vs. Net Income.

When the home office deduction is calculated correctly, it will only add up to this amount if the business has very little revenue. But if it does exceed your profit, you may carry over this loss into the following year.

How does home office deduction depreciation work for mortgage holders?

Unlike renters, mortgage holders must calculate their home office deduction using depreciation. Here’s how to go about it:

– Start with the smaller value of what you paid for the home and the current fair market value

– Add the cost of your improvements

– Subtract the value of the land

– Multiply that by the percentage of the home used for business

– Divide this by 39 (this is the IRS standard number of years to consider when depreciating the value of a home)

– The result is the depreciation value you may claim in a year

– For example, you would be able to deduct $705 as a depreciation expense against your home office in the following deduction:

– Purchase price: $300,000

– Fair market value: $325,000 (note, we won’t use this figure since it’s higher than the purchase price)

– Cost of improvements: $25,000

– Value of land: $50,000

– Proportion of home office: 10%

Cost basis: $300,000 + $25,000 – $50,000 = $275,00.

Tax deduction basis: $275,000 * 0.10 = $27,500

Annual deductible depreciation: $27,500 / 39 = $705

Which is Worth More, the Simple or Real Expense Deduction?

What’s right for you will come down to your particular circumstances.

Depending on your home office size and market (i.e., a high rent, metropolitan area), the real expense method can be higher than the $1,500 maximum allowed by the simplified safe harbor method.

But gathering the information to make that comparison can be tricky.

Luckily, there’s a way straightforward way to check if going through that process is worthwhile in the first place.

Do the real expense deduction math for only your rent costs (or depreciation costs if you’re a mortgage holder). Since the lion’s share of home costs come down to rent/mortgage payments, if that figure is relatively close to $1500, the real expense method is likely worth a larger deduction than the simple.

Otherwise, take the simple deduction.

Required Documentation

Maintaining proper documentation is crucial to substantiate your home office tax deduction. Here are some essential records you should keep.

Home Office Expenses: Keep receipts, invoices, and bills related to your home office expenses. This includes utilities, maintenance costs, insurance payments, supplies, and any repairs or improvements made to your home office space.

Proof of Exclusive Use: Provide evidence that your home office is used exclusively for business purposes. This can include photographs, a floor plan highlighting the designated office area, or any other documentation that supports your claim.

Tracking business expenses is tedious but essential not only for tax purposes but also so that you know whether you’re headed in the right direction.

For more information, read indinero’s ultimate guide to business tax deductions or how to track business expenses as efficiently as possible.

Conclusion

Maximizing the home office deduction means doing the math for the simplified and real expense methods detailed above and choosing the higher value.

The most challenging part is gathering accurate information about your home’s cost, depreciation, and miscellaneous home expenses, which may count towards the deduction. Indinero’s business tax services can take this off your plate. We’ll maximize your deductions, implement an accounting system that makes record keeping a breeze, and protect you from IRS audits. Contact us today.

{kind=link}