This may not be the most fun part of starting a business, but it shouldn’t be painful either. If terms like S corp, C corp, and sole proprietorship make your head spin, you’re definitely in the right place. This article will help you choose between a Sole Proprietorship vs LLC as well as provide a comparison of the five most common business organizations in the United States.

Your choice of business entity depends on a variety of factors including size, number of owners, optimal tax considerations, liability, and options available for raising investment capital. No matter what choice is right for you, Indinero provides expert business tax services that simplify the complex.

Let’s dive in.

Table of Contents

The Most Common Business Organizations in the United States

The most common business organizations in the United States are sole proprietorships, general partnerships, limited liability corporations (LLC), S corporations, and C corporations. Here are the basics you need to know about each.

Sole Proprietorship

Nearly all entrepreneurs start here.

If you’re doing business, you’re automatically considered a sole proprietorship, even if you don’t formally file yourself as a business. With this business type, there is no legal distinction between you and your business. Any profit ‘flows through’ to your regular income tax, and you are personally liable for debts or lawsuits should they occur.

You may take business loans in your personal name or use your personal credit cards to invest in the business. Be careful though—you’re liable to pay back those funds regardless of how the business goes. Assets like your car, home, or other securities are at risk of being seized should you go into debt from your business and aren’t able to pay it back.

General Partnership

A general partnership is identical to a sole proprietorship except for one major difference: instead of operating on your own, your business will have additional partners. It is assumed that profits will be split evenly unless otherwise agreed upon by all parties and documented accordingly.

Limited Liability Corporation (LLC)

An LLC is a formal legal entity separate from yourself. What this means is that your personal assets are immune if the business is sued or goes bankrupt. Only the money you choose to invest is at risk. Additionally, the business is also protected from your personal liabilities in the same way you are from the business.

Put another way, the liability protection of an LLC allows you to take more risk than you otherwise would. Investing in your business with a bank loan or credit card is easier when you aren’t personally liable if things go poorly.

An LLC does not pay corporate tax on profits, but income does flow through to your personal income tax bill. In addition to personal income tax, owners are responsible for paying Social Security, Medicare, and state and local taxes. The IRS requires quarterly filings.

You may deduct business expenses from revenue before calculating income taxes; the IRS defines valid expenses as both “ordinary” and “necessary”. For more details on valid and invalid business expenses, read these articles about small business taxes for beginners, thirteen business expenses you cannot deduct, or speak with an Indenero expert directly.

The legal protection an LLC provides is strong. Cornell Law writes that to justify revoking that protection, “…courts typically require corporations to engage in fairly egregious actions.” Examples include:

- If you personally injure someone

- Fail to pay taxes which were withheld from employees

- Commit fraud or something otherwise intentional and illegal

- Mix your personal and business expenses

The most common reason liability is repealed is because of the mixing of personal and business expenses. Avoiding this, in principle, means keeping separate business debit and credit cards and maintaining diligent records of business expenses and income.

Limited Partnership

Limited partnerships can be thought of as a hybrid between an LLC and a general partnership. In this case, some partners enjoy the legal protection of an LLC, while others do not. A limited partner must be passive; they may not participate in the management of the company in order to enjoy liability protection.

C Corporation (C Corp)

A C corp is a legal entity that is separate from its owners. It has two major unique characteristics that set it apart from other types of business entities: double taxation and stock equity. C corps pay federal corporate income tax on profits; shareholders must also pay taxes on any dividends they receive. The trade-off is that owners are permitted to raise capital by selling stock in the company. This entity is used by companies planning to go public.

S Corporation (S Corp)

An S corp is another type of legal entity that provides liability protection to its owners. This type of company passes income through to owners, like an LLC, and is not responsible for paying corporate income tax. To qualify for this special S-designation, the corporation must have no more than 100 shareholders (all of who are US citizens) and issue only one type of stock.

A comparison of the most common business entities in the United States:

| Ownership | Formation | Owners Personally Liable? | Taxes | Raising Funds | |

| Sole Proprietorship | One person | No filing necessary | Yes | Personal Income | Personal credit; no stock |

| General Partnership | At least two | No filing necessary | Yes | Personal Income | Personal credit; no stock |

| Limited Liability Company | At least one | Must file;

~$100-$200 | No | Personal Income | Business credit; no stock |

| S Corporation | At least one; maximum 100 | Must file;

~$800-$3000 | No | Personal Income | Business credit; can sell stock |

| C Corporation | At least one | Must file;

~$800 | No | Company pays corporate tax rate; shareholders pay personal income tax on distributions | Business credit; can sell stock |

How to choose your small business entity

Choosing a small business entity is no easy task. It has important implications for the future of your business and deserves appropriate consideration.

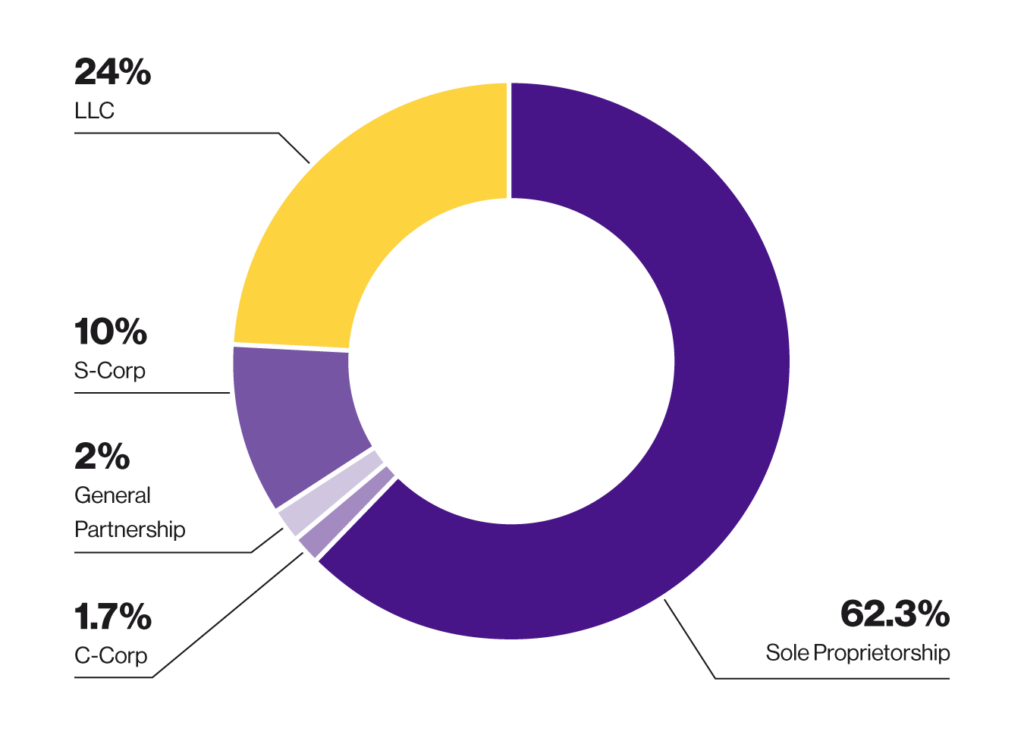

To give you an idea of the decisions other business owners make, here is the US Census proportional breakdown of business organizations. If you’d like to speak to an expert about which choice is best for your unique business, you can book an appointment with us.

Let’s take a closer look at these different business structures, side by side, to help you make the right choice.

Sole Proprietorship vs LLC

When evaluating Sole Proprietorship vs LLC, the biggest difference is the liability protection afforded by an LLC; personal assets are shielded from business liabilities, which is not the case for sole proprietorships. Additionally, sole proprietors will find it more difficult to secure bank loans, which is likely easier for LLCs.

For tax purposes, both entities have profits flow through to the owners as regular income by default, and both must pay Social Security and Medicare taxes. However, when considering an LLC vs sole proprietorship, the LLC has the advantage of being able to choose to be taxed as an S corp. In this case, the LLC owner may choose the S corp designation because they won’t be required to pay Social Security and Medicare taxes on income passed through to them.

There is a small drawback to LLCs: it costs money to file with the state and requires the ongoing diligence of separating business and personal expenses to maintain liability protection.

Even if you feel it isn’t time to file your business as an LLC because you have low to no revenue, it is still worthwhile. Establishing your LLC means you can begin building a credit history in your business name. This way, in the future you’ll be eligible for loan opportunities that are unavailable to newly formed LLCs.

S Corp vs LLC

S corps have advantages over LLCs in two important ways: the tax treatment of pass-through income and raising capital through the sale of stock.

Income passes through from the company to the owners in both cases. But income passed through to an LLC is subject to Social Security and Medicare taxes, while distributions passed through an S corp are not.

Secondly, LLCs can technically sell equity in the company by bringing on additional partners. However, S corps are more attractive for companies looking for venture capital, because they are permitted to sell equity ownership through stock whereas LLCs are not.

Other differences when comparing an LLC vs S corp include that S corps may have no more than 100 shareholders, their owners must be US citizens, and they may not be owned by another legal entity. Notably, maintaining S corp status is both more costly and carries more regular and expensive filing requirements with the state.

Lastly, the company management teams differ as well. An S corp is owned by shareholders and managed by a formal board of directors, while an LLC is owned and managed by its owners.

Both business structures feature separate legal entities between owner and company, liability protection, pass-through income taxation, and ongoing filing and compliance requirements with the state.

Note: There is no requirement to register your business in your home state. Since each state has different rules, where to register is an important consideration as well. If you aren’t sure, speak with a tax specialist.

C Corp vs LLC

The two largest differences between LLCs vs C corps have to do with how the corp is taxed and the options available for raising funding.

C corps must pay federal corporate income tax while LLCs, assuming they don’t elect to be taxed as a C corp, do not. In other words, they are subject to double taxation. This drawback is made up for by the fact that C corps are able to issue equity through the sale of stock. This makes the corporate entity more attractive to venture capitalists since it can sell stock while an LLC cannot.

A final consideration when considering an LLC vs C corp is that the latter is more expensive to register and legally maintain than the former. Additionally, management of the companies differs as well. LLCs are run by the owners while C corps are owned by shareholders and managed by a board of directors.

S Corp vs C Corp

The default type of corporation is a C corp. To become an S corp you must file for a special designation in addition to incorporating. A C corp is unique compared to the entities covered so far in that it faces double taxation. It must pay both corporate taxes on profits as well as personal income tax on dividends.

On the other hand, an S corp is a pass-through entity that is taxed similarly to an LLC. Earnings are distributed and owners pay regular income tax. This is why there are considerably more S corps than C corps; if a company meets the requirements, then they enjoy the benefit of not paying corporate income tax. Additionally, shareholders are not responsible for paying Social Security and Medicare taxes on distributions.

The requirements to file as an S corp are:

- No more than 100 shareholders; each must be an individual US citizen, trust, or estate

- Incorporated domestically

- There may be only one type of stock issued. The stock is identical in terms of voting rights, distributions, and liquidation proceeds

- Use a calendar year, instead of a fiscal year, for tax purposes

- Shareholders must unanimously choose to file as an S corp

- Cannot retain earnings; profits must be distributed to shareholders

Despite S corp tax benefits, there are scenarios where C corps are the better choice. C corps are more flexible to owners and investors because they can issue multiple types of stock. Secondly, since there is no maximum number of shareholders, a C corp is appropriate for a company that plans to go public. Lastly, C corps are able to deduct fringe benefits, such as health insurance, disability insurance, and life insurance while S corps cannot.

Conclusion

The choice of which business entity to form requires careful consideration. There are good arguments for or against each possibility. If you’d like to focus on what you do best and let us advise on and take care of these details for you, book a conversation with an Indinero expert.

{kind=link}