When you decided to pursue a career in the non-profit sector, you unlikely wanted to do nonprofit accounting work.

It’s hard to feel the difference you’re making if you spend the day on spreadsheets and compliance. Fortunately for you, it’s common practice for small and large organizations to outsource to outside accounting firms or volunteers.

But before you delegate or take on this task yourself, it’s important to have a high-level understanding of accounting for nonprofit organizations.

This article is an introduction for non-financial professionals. When you’re finished, you’ll understand what internal and external stakeholders care about and have a foundation in the language of finance you can use going forward.

If you have specific questions about your organization’s accounting or bookkeeping, contact the indinero accounting services team today.

Debunking 4 Myths About Outsourced Accounting

What Is Nonprofit Accounting?

Financial statements, bookkeeping processes, and compliance standards are similar for both businesses and nonprofits. Internally, they’re used for planning and evaluating how long an organization can stay in operation. The key difference is that, externally, they serve different stakeholders with different goals.

Instead of demonstrating shareholder value, nonprofit accounting is geared towards accountability and proving the impact of donor and grant dollars.

This comes with an accounting practice unique to the nonprofit industry. Since money can be donated or granted on a restricted basis, nonprofit accounting separates these assets and revenues into distinct categories.

Quality accounting is directly related to earning and retaining donors and grant funding. Not only do most grants require Generally Accepted Accounting Principles (GAAP) to be followed, but transparency also builds trust with donors. Quality accounting leads to high-value impact reports, cementing relationships with existing donors and potentially persuading new ones.

Nonprofit accounting centers on the following principles:

- Generating financial reports with bookkeeping data.

- Using internal reports to evaluate the financial health of your organization.

- Presenting reports externally to demonstrate impact, prove funds are being used responsibly, and uphold IRS compliance.

- Maintaining grant eligibility and demonstrating accountability through GAAP compliance.

Accounting vs Bookkeeping

Let’s begin by clearing up a common misconception: accounting and bookkeeping aren’t the same thing.

We cover this topic in-depth in our article Bookkeeping vs Accounting, but the difference comes down to these key points:

- Bookkeepers are responsible for managing and recording transactions on a day-to-day basis. Duties include “balancing the checkbook” with regular bank reconciliations, preventing the commingling of funds, and running payroll.

- Accountants manage finances on a long-term basis. They gather the information bookkeepers produce, generate financial reports, and produce analyses that guide decision-making.

Every organization needs a bookkeeper, but only some need an accountant. Duties sometimes overlap and can be performed by the same person, but accounting requires higher levels of education and training.

Internal vs External Stakeholders in Nonprofit Finance

Nonprofit organization accounting can be categorized according to internal and external stakeholders.

Internal Stakeholders

Internal stakeholders include the nonprofit board, executives, and employees. These individuals are chiefly concerned with an organization’s impact and overall financial health. “Impact” is a loose term that is specific to a nonprofit’s unique mission.

The goal of nonprofit accounting is to connect “impact,” as defined by a nonprofit, with the concrete record-keeping and reporting requirements of GAAP accounting. When done correctly, one can draw a direct line between the funding an organization receives and the change it creates in a community.

Evaluating an organization’s “financial health” is a complicated conversation. For our purposes, we’ll simplify the topic. John Zietlow, professor of nonprofit financial management at Indiana University, emphasizes one key criterion in his teaching: Does the organization have at least six months of operating expenses available?

Even though they aren’t businesses, nonprofits can own any number of assets: real estate, stocks, and bonds are a handful of examples. However, having six months of operating expenses available means that those funds must be liquid. That means cash, pledged donations one has not yet received, lines of credit, or other funding sources accessible in a short time frame.

Once an organization establishes its six-month safety net, it should consider investing further into either fundraising or directly achieving its mission.

External Stakeholders

Eternal stakeholders include many individuals and entities, including donors, potential donors, grantmakers, the IRS, and the general public.

Donors and potential donors look for clear and accurate financial statements, evidence of prudent spending, and assurance that their funds are being used responsibly and effectively. Transparent accounting allows them to evaluate an organization’s financial health and accountability before contributing.

Grantmakers, including governments and private foundations, have specific requirements for using the funds. This is one of the reasons fund accounting is so important to the industry. Accurate accounting fulfills these obligations and enhances the likelihood of future funding.

There are many requirements for maintaining 501(c)(3) nonprofit status. While nonprofits don’t (usually) pay taxes, the IRS does require them to file an informational Form 990, providing detailed information on the organization’s finances. This information is publicly available.

What is GAAP?

GAAP is important to nonprofits because grantors often require it for eligibility. The Generally Accepted Accounting Principles (GAAP) are guidelines developed by the Financial Accounting Standards Board to ensure that financial statements are complete, consistent, and comparable.

GAAP accounting is complex for non-financial professionals for various reasons, but the largest one is that transactions are recognized on an accrual basis rather than a cash basis.

You’re likely familiar with cash accounting; it’s how household budgets are run. Money is recorded as it comes in and out of your bank. On the other hand, accrual accounting records these sales or services as they are earned, spent, or performed, whether actual payments are received or not.

For example, if you use the cash method for your accounting and receive a multiyear grant that pays a lump sum once a year, each payment would appear as a single sum the month the grant money is paid. If you’re using accrual, the grant would be broken into monthly (or smaller) increments for accounting purposes.

GAAP and accrual accounting are more complicated but also more accurate and transparent.

Simplify GAAP Compliance With Our Essential Checklist

Essential Financial Documents and Reports

Even though nonprofit accounting doesn’t involve equity or shareholders, it’s still complicated. Managing your finances and transparently reporting where you stand to stakeholders requires quite a few documents:

- The Internal Budget is a forward-looking document that guides your internal decision-making. Revenues and expenses are estimated, and the document is updated continuously as conditions change.

- The Statement of Financial Position, also called a balance sheet, provides a static view of assets and liabilities.

- The Statement of Activities, also known as an income statement, is a backward-looking document that shows revenues and expenses over a given period.

- The Statement of Cash Flow, similar to the statement of activities, is a backward-looking document that shows revenues and expenses. The difference is that a cash flow statement concerns money that moved into or out of the organization, while a statement of activity uses accrual-based accounting.

- The Statement of Functional Expenses is a detailed view of expenses by function.

Let’s take a deeper look at each of these.

Internal Budget

Unlike financial statements that report past performance, the budget helps an organization plan for the future by setting financial goals and allocating resources accordingly. The budget includes estimates of all expected sources of income, such as grants, donations, membership fees, and fundraising events, alongside anticipated expenses and operational needs.

A strong understanding of financial modeling is crucial for building an internal budget. It’s good practice to plan for both best- and worst-case scenarios and construct contingency plans, allowing you to react quickly to changing circumstances.

Regularly monitor and update as needed.

Statement of Financial Position

This document lists an organization’s assets (what it owns) and liabilities (what it owes). Net assets are listed as the sum of these and broken into unrestricted, donor-restricted, and partially restricted assets. It’s standard practice to report two years of financial positions so that stakeholders can compare and examine trends over time.

Examples of assets include:

- Cash

- Stock equity

- Accounts receivable

- Real estate

- Prepaid expenses

- Equipment

Examples of liabilities include:

- Accounts payable

- Debt

- Grants payable

- Wages payable

- Deferred revenue

- Interest payable

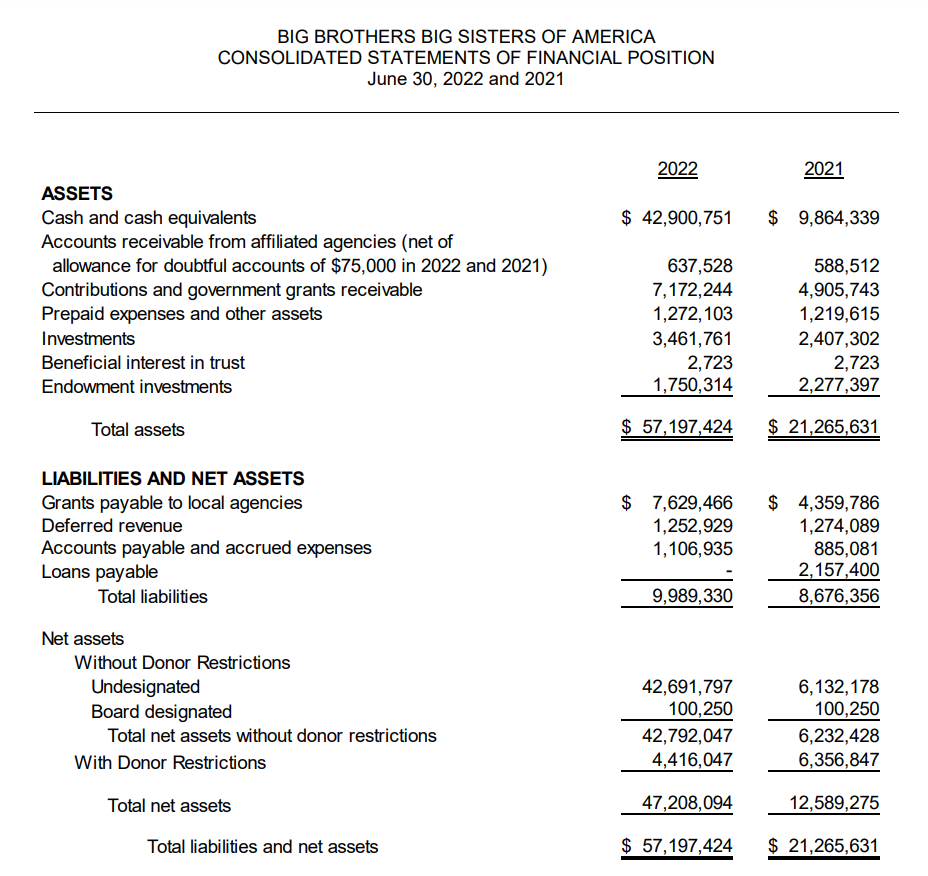

Statement of Financial Position Example

Here’s a real-life example: Big Brothers Big Sisters of America 2022 consolidated financial statements. It’s important to note that this is the final product of an in-depth accounting and bookkeeping process, incorporating data from many sources. Without quality bookkeeping, none of this is possible.

While GAAP reporting includes a considerable number of standard conventions and expectations, accountants have the freedom to include sometimes unique line items. In this case, the assets section specifically includes a line for “doubtful accounts,” which the organization doesn’t expect to collect.

A stakeholder will first notice that net assets increased considerably between 2021 and 2022, owing to a significant increase in cash. As a hypothetical executive of Big Brother Big Sisters, it will be important for you to have an explanation for stakeholders who are wondering what that money will be used for.

| Looking for a deeper dive? Read our article on the nonprofit statement of financial position. |

Statement of Activities

The statement of activities, also called a profit and loss statement or income statement in the for-profit world, details revenues, expenses, and changes in net assets over a specific period. It helps stakeholders understand how the organization’s funds are being used and evaluate the health of a nonprofit by looking for surpluses or deficits.

Revenues and expenses are categorized according to their source—for example, donations, grants, program fees, or fundraising fees. This document allows you to connect the costs to your impact on your mission. Since mission-related data is so variable and subjective, it won’t be collected for financial statements, but it’s necessary to collect that information to present in impact reports.

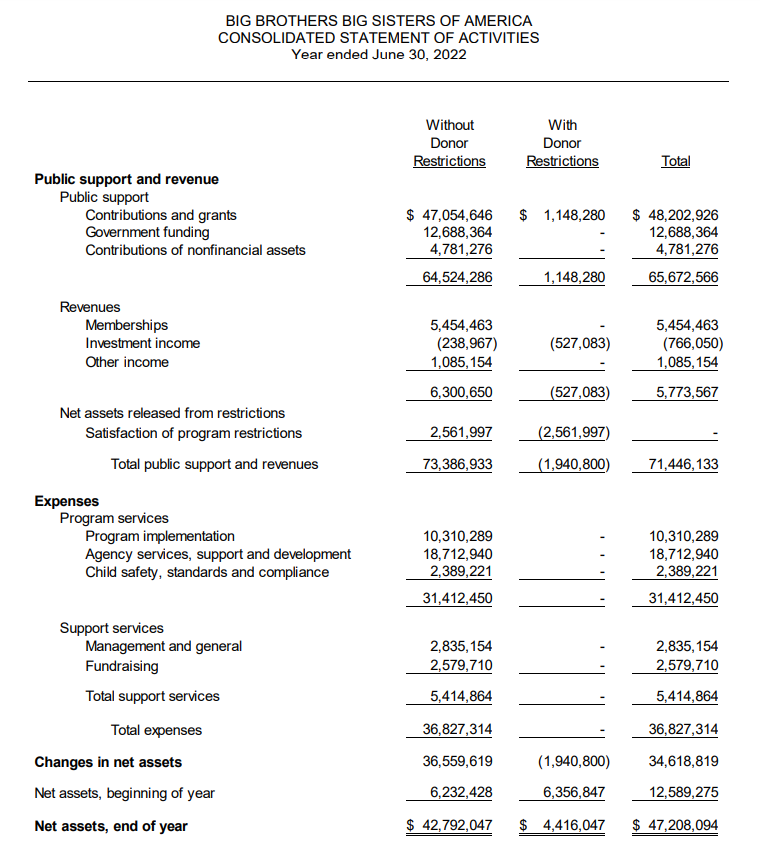

Statement of Activities Example

You’ll notice that revenues are divided into restricted and unrestricted funds, just like in the statement of financial position. The spreadsheet is too large to show two years at once, but stakeholders will want to compare, so the 2021 and 2022 statements are presented side by side in the source material.

Examining the 2021 and 2022 statements, you’d see a considerable increase in contributions and grants. This is great news for the organization and worth highlighting in donor communications and annual reports.

Statement of Cash Flow

Of the statements discussed here, the cash flow statement is the most important for managing internal finances. The only way to maintain six months of expenses is by managing the cash balance appropriately.

The report is divided into three sections: operating activities, investing activities, and financing. Donations and payments to suppliers are considered operational activities, investing activities concern purchasing real estate or equipment, and financing relates to borrowing or repaying loans.

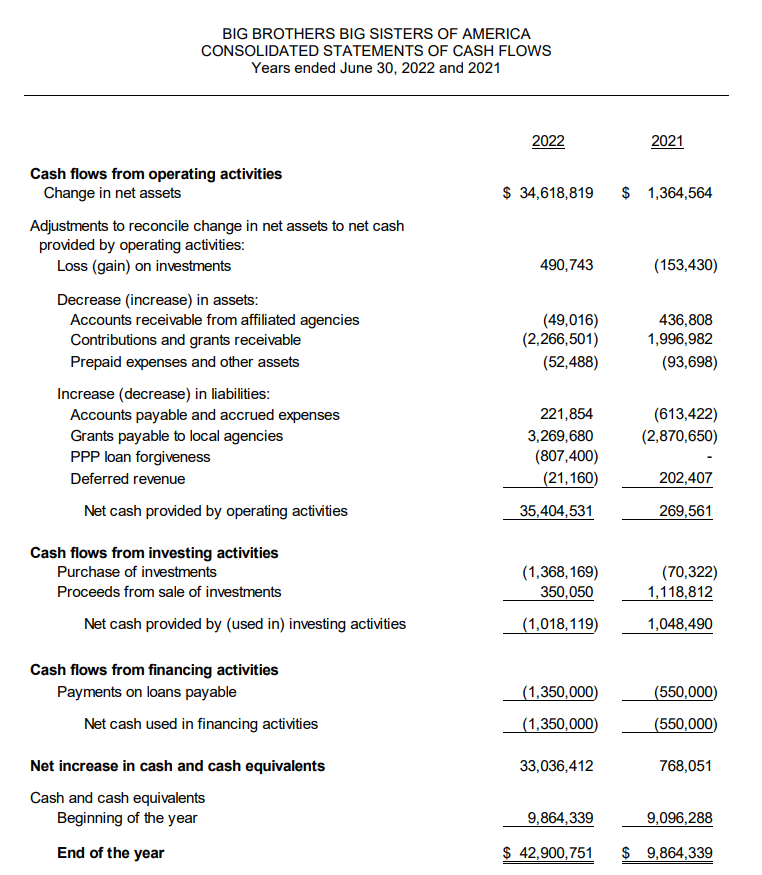

Statement of Cash Flows Example

Similarly to other statements, the cash flow report shows two years’ worth of information, allowing stakeholders to evaluate trends.

The Big Brothers Big Sisters cash flow statements contain some important information; the “change in net assets” figures match with the statement of activities statement. Normally, grants and large donations would be made over years and thus would only be partially reflected on the cash flow statement. In this case, the entire sum appears in the 2022 column, meaning this was a one-time lump sum. This scenario provides considerable flexibility to executives managing the organization.

Statement of Functional Expenses

The statement of functional expenses is unique to nonprofits. While for-profit companies might have an internal document that divides spending across departments, the nonprofit sector is required to break this information down.

Common categories include program implementation, administrative support, outsourced services, and fundraising. These categories are further divided according to how that money was spent: for example, salaries, taxes, insurance, and grants to other agencies.

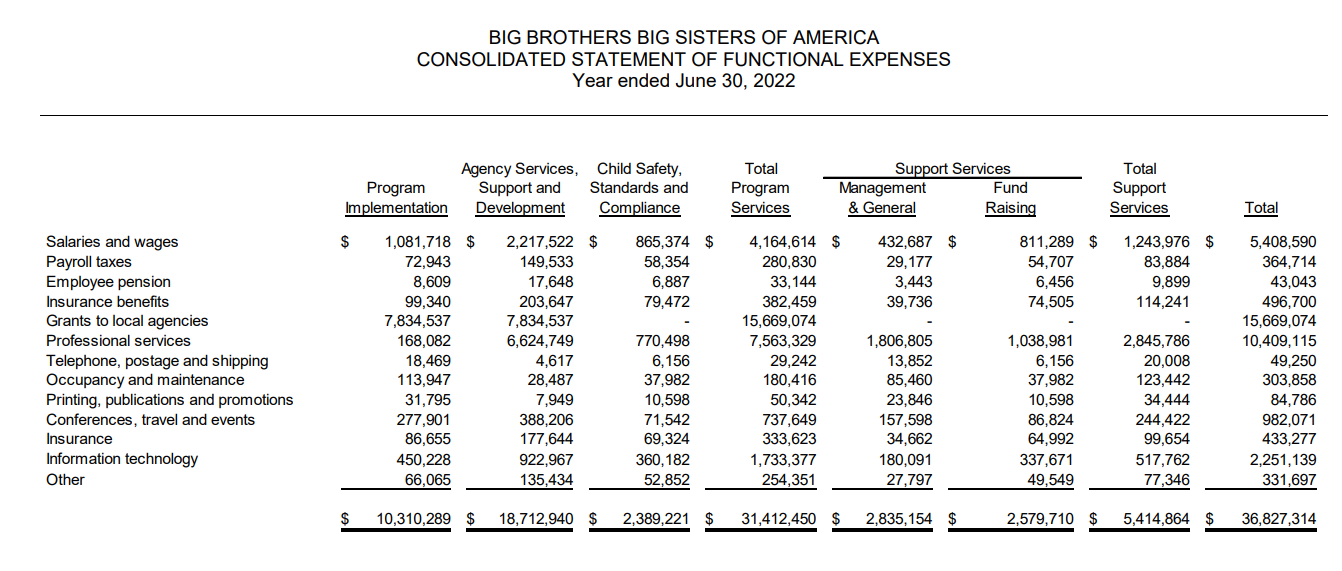

Statement of Functional Expenses Example

Donors are notorious for not wanting to spend money on administrator salaries. While these personnel are essential, supporters want to see that their money is going specifically toward the programs that serve the nonprofit’s mission. The Big Brothers Big Sisters statement of functional expenses demonstrates this nicely, with $31,412,450 going toward community programs while only $5,414,864 is dedicated to support services.

Relevantly, comparing this statement with the cash flow statement allows one to easily evaluate liquidity levels. In this case, the Big Brothers Big Sisters spent ~$36 million while they have a cash balance of approximately the same size. Since they have well over six months of expenses in reserve, they’re certainly in a financially healthy situation.

Form 990

Other than organizations with less than $50,000 in annual revenue, it is standard procedure for nonprofits to file a Form 990 with the IRS. This is part of their compliance requirements for maintaining 501(c)(3) status.

Once the above statements are generated, the Form 990 is easy to complete. It isn’t required to be GAAP compliant or to detail donor-imposed restrictions.

| Many nonprofits are grant-giving organizations but don’t extensively advertise. For nonprofits seeking funding, working backward from publicly available Form 990 information is a great way to discover potential fundraising sources. |

Who Does the Accounting?

Small nonprofits often rely on a bookkeeper who may be a part-time staff member or volunteer, such as the board treasurer. While this approach keeps costs low, it can lead to issues with accuracy, timeliness, and the overall usefulness of financial reports.

An alternative is outsourcing some or all accounting and bookkeeping tasks to a professional firm. Although outsourcing can be more expensive, the benefits of improved accuracy, timely reporting, and higher-quality financial management can outweigh the additional costs.

If you choose to DIY your accounting, implement a system for tracking expenses. Since it’s automated and connected to your bank account, QuickBooks is one of many software solutions that can make your job easier.

Nonprofit Accounting Best Practices

Nonprofit accounting involves more than tracking income and expenses; it requires a strategic approach to financial management, accountability, transparency, and sustainability. Here are some recommended best practices for your organization:

- Set and maintain a cash reserve target. Six months of expenses is the most commonly recommended amount of time.

- Avoid accumulating too many funds. Maintaining an appropriate cash reserve is important, but it’s equally important to actually use the money that has been granted or donated to your organization.

- Switch from cash to accrual accounting as soon as possible. While cash accounting is easier, accrual is more accurate. It allows you to plan your finances better while presenting an accurate picture to donors.

- Just as entrepreneurs should keep personal and business finances separate, nonprofits should have a method of separating funds donors have restricted for specific purposes. The best method is to maintain separate bank accounts.

- Segregating bookkeeping and accounting duties is crucial for preventing fraud. If one person is in control of the finances, they have the opportunity to misuse funds. Since more people will review finances, this also helps prevent honest mistakes.

Conclusion

Whether directly involved in accounting or outsourcing to a third party, knowing these fundamentals helps align financial best practices with your nonprofit’s mission.

If you’re considering outsourcing your accounting or bookkeeping duties, contact an indinero accounting services team member. We have a long history of serving nonprofits and provide flexible plans tailored to your organization.

{kind=link}