A nonprofit statement of financial position is one of several documents nonprofits can use to demonstrate where donors’ money is being spent. It’s essential for nonprofits looking to grow—but they can be complicated.

In this guide, we’ll teach you the core components of the nonprofit statement of financial position and how to put one together in a way that’s as painless as possible. We’ve also provided an example nonprofit statement of financial position to guide you.

If your nonprofit needs assistance putting together a financial statement or simply managing funds, indinero’s accounting services team is here to help. Our experts have extensive experience in the non-profit sector and are a more affordable option than a full-time employee or team.

Table of Contents

Statement of Financial Position vs Balance Sheet

A statement of financial position is simply another term for a balance sheet; there is no difference. It reports an organization’s assets, liabilities, and net assets at a set point in time.

Why Is a Statement of Financial Position Important?

Charitable organizations may not pursue financial gain, but that doesn’t mean they don’t need funding to operate and further their cause. Without surplus revenue, a nonprofit can’t grow or scale its mission.

Not-for-profit organizations have a fiduciary responsibility to show their donors what their finances look like at the end of each fiscal year. Also, well-organized financial documents are necessary to understand the health of a nonprofit.

The standard reporting procedure is to include end-of-year balances for at least two years so donors can see trends and measure the present moment.

What Is the Most Difficult Part of Preparing the Statement?

Having a proactive system for tracking the movement of funds during the year is the most difficult piece of reporting. Nobody wants to dig through the proverbial “shoebox” of receipts come reporting time. They’re a mess to untangle.

Read our article on tracking business expenses; much of our guidance is transferable to nonprofit operations.

Core Components

When it’s all put together, a nonprofit statement of financial position is a pretty straightforward document. Putting it together, however, can take time because there are a number of essential components you or your accounting expert will need to assemble.

Here’s what those are:

List of Assets

Your financial position statement must show the assets your non-profit owns or controls. In this case, assets are any resources owned by an organization that are expected to generate future economic benefits. They are classified into two primary categories: current assets and noncurrent assets.

Current assets are resources that can be utilized or converted into cash within one year or the normal operating cycle of the organization, whichever is longer. They include:

- Cash and Cash Equivalents

- Accounts Receivable

- Prepaid Expenses

Non-current or long-term assets are resources an organization uses to support its mission for over a year. They include:

- Property and Equipment

- Investments

Liabilities

Liabilities are financial obligations that must be fulfilled in the future and part of the full picture you’re drawing on your nonprofit statement of financial position. Liabilities are also divided into two categories:

Current Liabilities are obligations expected to be settled within one year or within the normal operating cycle of the organization. They include:

- Accounts Payable

- Grants Payable

Non-Current Liabilities are obligations that extend beyond one year. They include:

- Long-Term Debt

- Pension Obligations

- Mortgages or Leases

Understanding Net Assets

As with the for-profit sector, net assets represent the financial resources available to an organization after deducting liabilities. This figure should also be included in the statement.

Example Nonprofit Statement of Financial Position

We’ve created an example below to show you what a nonprofit statement might look like.

Read through it and see if you can draw any conclusions about Acme Nonprofit’s current financial status. Afterward, we’ll walk through what a donor might think when reviewing this information.

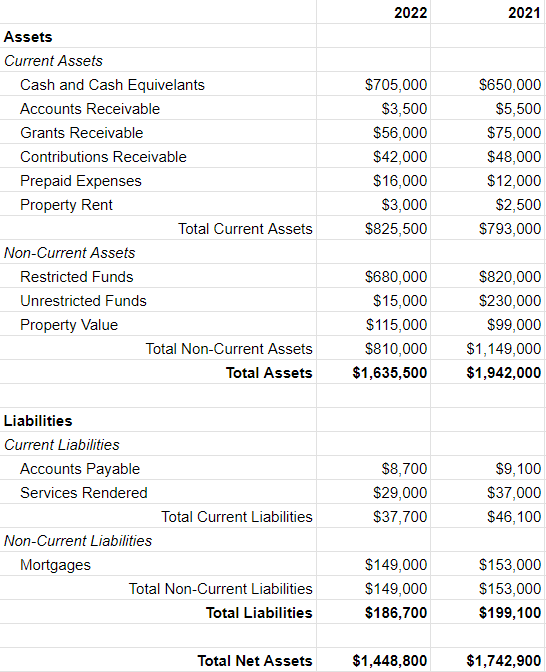

Acme Nonprofit

Statement of Financial Position as of June 30, 2022 and 2021

Analyzing the Statement

When preparing your year-end impact reports, you can anticipate how your balance sheet may be perceived and incorporate that into the narrative.

There’s a lot of exciting information to learn about Acme Nonprofit from this balance sheet. Did your analysis reveal anything similar?

- The organization has positive net assets, meaning they are “solvent.” This is a sign of financial health.

- Despite being liquid, the magnitude of non-current assets decreased considerably. No investment assets are listed, so the funds weren’t used to purchase equities. Donors might question where the money ended up or voice concern that something happened.

- The organization’s cash position increased despite drops in both accounts and grants receivable. Why? It’s impossible to know for sure without examining a statement of cash flows, but likely explanations are cuts in staffing or mission-related expenditures.

- The industry standard is to keep ~6 months of operating expenses in liquid assets. Acme has ~$825,000 in current assets at its disposal. This may be a lot or a little, depending on the organization’s level of expenses. After reading this, donors would likely want to examine Acme’s cash flow statement to find out.

- The value of the organization’s property increased, likely due to the economic tailwinds between 2021 and 2022.

The last thing to note is that gaining a comprehensive picture of a nonprofit’s accounting and financial health relies on more than the snapshot a balance sheet provides. Reading and understanding other financial documents, briefly covered below, is necessary to fill the gap.

| Important note: Balance sheet composition will differ based on whether one chooses the cash or accrual accounting method. GAAP compliance requires organizations to use accrual accounting, recognizing expenses when they occur rather than when cash changes hands. Learn more about accrual accounting in our guide to GAAP principles. |

What Other Nonprofit Financial Statements Are Important?

In addition to the nonprofit statement of financial position, organizations should prepare the following statements to comply with GAAP principles:

- Statement of Financial Activities reporting revenue, expenses, and activities with and without donor restrictions

- Statement of Functional and Natural Expenses showing expenses by function (i.e., program, fundraising, and administrative) and nature (i.e., supplies, marketing, and salaries).

- Statement of Cash Flow showing how cash circulates in three main areas: investing, financing, and operation.

Conclusion

A nonprofit’s statement of financial position, or balance sheet, provides a snapshot of an organization’s assets, liabilities, and net assets.

Having individuals with expertise in composing, reading, and analyzing balance sheets is important to fulfilling a nonprofit’s mission. If your organization needs such expertise, consider hiring indinero’s accounting experts. We’ll provide expertise at a fraction of the cost of a full-time employee or in-house team.

{kind=link}