Issuing restricted stock is a common way to compensate a company’s founders. If you are a founder of a new business, an 83b election is a vital tax form that can save you serious money when it comes time to file taxes. An 83b filing could work out great for you, but the ins and outs of this form can be confusing, leaving founders and tax preparers alike unsure of what to do.

The good news is that the IRS 83b form is easy enough when you know how and when to file it. Read on for a quick guide to 83B and why your startup needs to know about it.

What Is 83b?

Being paid in restricted stock is a common practice in the world of startups. Just like any other form of payment, you have to pay tax on it. The 83b election form is a letter you send to the IRS to let them know you’d like to be taxed on shares of restricted stock—on the date the equity was granted to you instead of the date the equity vests.

You can only do an 83b filing for stock that’s subject to vesting. Grants of fully vested stock are taxed at the time of the grant.

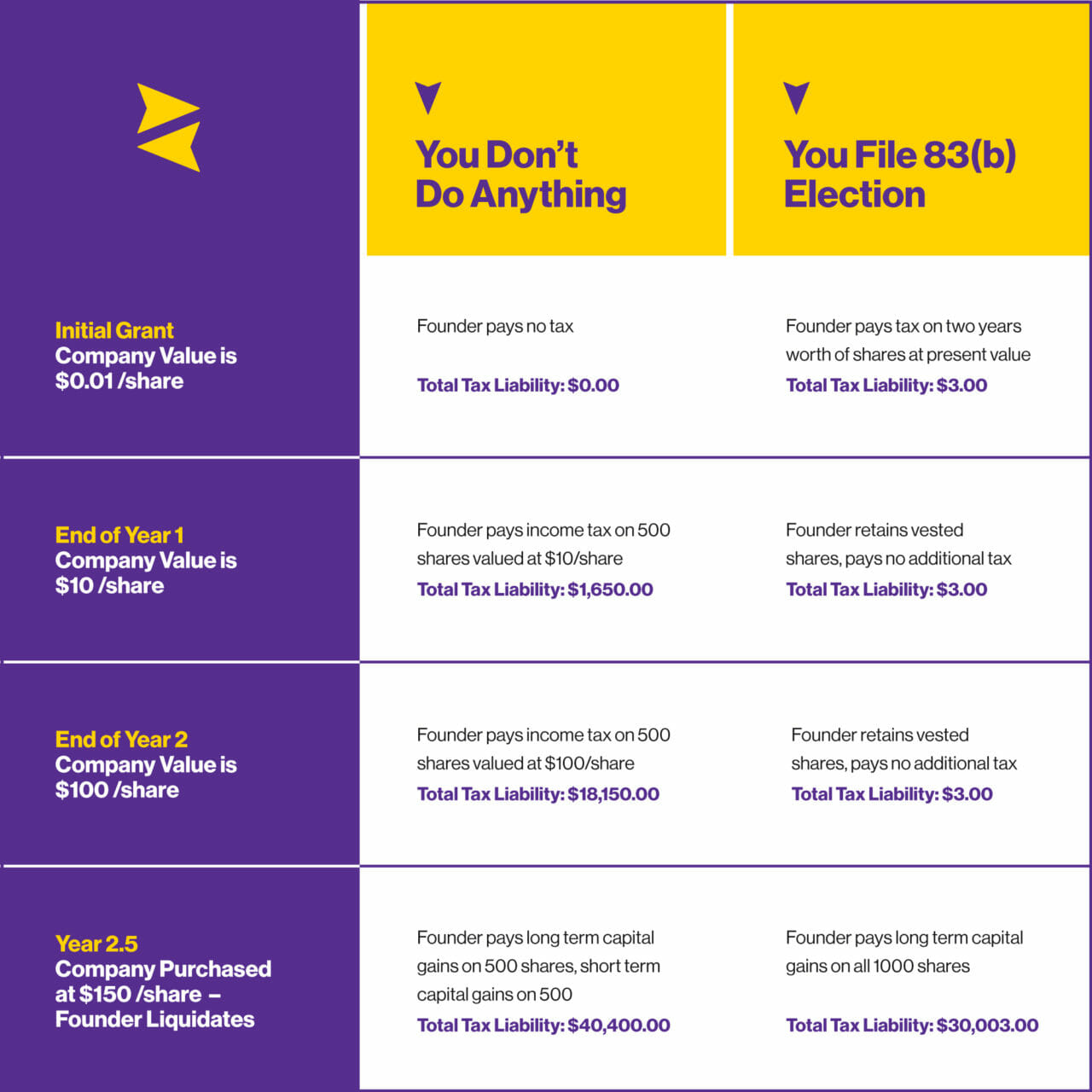

IRS 83b election: Low Initial Cost, High Eventual Payback for Founders

The 83b election lets you pay taxes on the total market value of your equity grant at the beginning of your vesting agreement, as opposed to paying taxes on it annually.

Using the 83B election means that if your stock explodes in value later on, you won’t have to pay an annual tax on it unless the company is bought, merged, or goes public. Even then, you won’t pay the typical income tax rate—you’ll pay the considerably lower long-term capital gains rate.

Obviously, the exact amount of tax savings will vary by situation. Still, it’s safe to say that shareholders whose companies are new and building value have everything to gain from the 83B election.

Use the Small Business Tax Election, Or Potentially Lose It

Certain situations benefit from using the 83b election more than others—such as a brand-new company in which the founder’s equity is humbly valued.

There is only one major risk to taking the 83b tax election. Because your stock could go down in value as opposed to up, you may lose money and save on taxes. This is why founders with a lower valuation tend to benefit the most from 83b.

Also, if you leave your company before your restricted stock vests, you’ll lose out on the tax money you paid when you filed the 83b election form.

When and How to Do an 83b Filing

You only have 30 days after the grant is made to tell the IRS that you will use the election. Missing the window for 83b filing can cost a startup’s founders a lot of money.

To do this, you will need to send the IRS a letter, and they’re going to want quite a few pieces of information to grant the election. To get an idea of what you’ll need to provide and see how your letter should be structured, check out this sample letter on the SEC website.

You’ll need to have three copies of your completed letter: The original goes to the IRS. One copy goes to the company. The other one stays in your personal records.

83(b) Tax Election for Foreign Investors

If you’re a foreign investor living in the United States (the IRS calls you a “nonresident alien”), you can still benefit from the 83b, but there are a few more things you need to know.

The IRS doesn’t explicitly state that a nonresident alien can or cannot file an 83b. So if you do file an 83b, you’re leaving yourself open to paying US income tax on the value of the stock, at least in theory. But if all the services you’ve provided to the company have taken place outside of the United States, you won’t need to pay tax on your equity.

If you’re a foreign investor who plans to become a resident alien, you will benefit from the 83b because the value of the stock at the end of the vesting period will not be taxed under the normal rules of §83, thanks to the previous 83b election that was made. However, you will have to pay tax on the stock when it’s sold.

Because foreign tax credits for the tax imposed on the stock transfer date would usually not be available to nonresident aliens, the 83b can help foreign investors with plans to become resident aliens avoid double taxation.

Your 83b Can Be Signed Electronically (For Now)

In late 2021, the IRS announced that it would temporarily allow a number of tax forms to be signed electronically instead of with a handwritten signature. The 83b IRS form is among the documents included on the list.

This is an extension of a pandemic-era policy adopted in 2020. As of this writing, the extension is set to expire on October 31, 2023. While this date may be extended again, check with your tax preparer or financial advisor to be sure.

Let indinero’s Accounting Team Help You Take Advantage of 83b

The 83b election is a great option for founders of brand-new companies, resulting in significant tax savings down the road. But you need to send an 83b filing at the right time to take advantage of its benefits.

The benefits of 83b election stock options are just one way to save the founders some serious cash. Fortunately, inDinero’s tax accountants are here to help you find the best options available. Reach out to us today to find out how!

{kind=link}